Mortgage Pre-Approval in 2026: Why Getting Approved Early Gives You a Competitive Edge

Navigating the Winnipeg Real Estate Market with Confidence

As we step into 2026, the real estate landscape in Winnipeg, MB continues to evolve. With fluctuating inventory levels and dynamic interest rates, waiting until you find your dream home to sort out financing is a strategy of the past. Securing a mortgage pre-approval is no longer just a preliminary step; it is a critical tool that provides a distinct competitive advantage.

Whether you are a First Time Home Buyer or looking to upgrade to a larger property, getting approved early establishes your budget and signals to sellers that you are a serious contender. As a Mortgage Specialist with over 20 years of experience, I have seen how a solid pre-approval can be the deciding factor in a multiple-offer scenario.

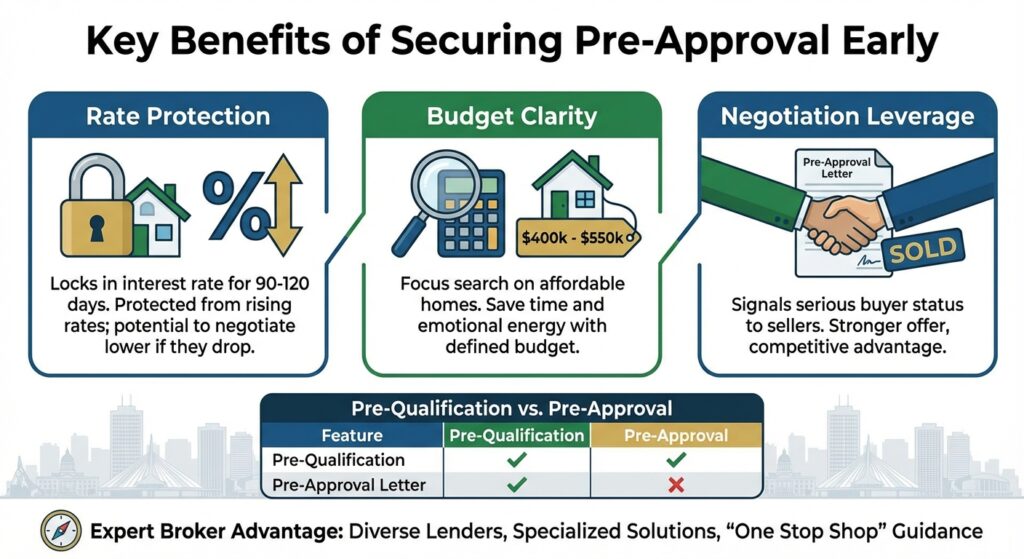

Key Benefits of Securing Pre-Approval Early

Getting pre-approved does more than just tell you how much you can borrow; it protects your purchasing power. Here is why you should prioritize this step:

- Rate Protection: A pre-approval typically locks in an interest rate for 90 to 120 days. If rates rise while you are shopping in Winnipeg, you are protected. If they drop, you can often negotiate the lower rate.

- Budget Clarity: It helps you focus your search on homes you can actually afford, saving time and emotional energy.

- Negotiation Leverage: Sellers prefer buyers with verified financing. A pre-approval letter from a trusted Winnipeg Mortgage Broker can make your offer as attractive as a cash offer.

Even if you have faced credit challenges or are self-employed, getting assessed early allows us to address any issues before they become roadblocks.

| Feature | Pre-Qualification | Pre-Approval |

|---|---|---|

| Depth of Review | Basic verbal overview | Detailed credit & income analysis |

| Verification | Unverified data | Verified documentation (T4s, Paystubs) |

| Rate Hold | Rarely included | Yes (typically 90-120 days) |

| Seller Confidence | Low | High |

How an Expert Broker Makes the Difference

Many buyers assume they should go straight to their bank, but working with an independent broker offers more flexibility. I have access to a wide range of lenders and specialize in finding solutions for diverse situations, including mortgage refinancing and second mortgages.

If you have been turned down by a bank due to poor credit, minimal income, or self-employment, do not be discouraged. My goal is to be your “One Stop Shop,” helping you navigate the complexities of the 2026 market to save you time and money. By analyzing your unique financial profile, we can structure a mortgage product that suits your long-term goals.

Q1: Does a mortgage pre-approval guarantee I will get the loan?

A pre-approval is a strong indicator of your ability to borrow, but it is subject to the property appraisal and your financial situation remaining the same until closing.

Q2: How long does a pre-approval last?

typically, a pre-approval locks in your rate and amount for 90 to 120 days, giving you ample time to shop for a home in Winnipeg.

Q3: Will getting pre-approved hurt my credit score?

A pre-approval requires a hard credit check, which may temporarily dip your score slightly, but it is a necessary step for securing financing and is expected by lenders.

Q4: Can I get pre-approved if I am self-employed?

Yes! While banks can be strict with self-employed applicants, as a broker, I work with lenders who understand business income and can offer specialized solutions.

Q5: What documents do I need for a pre-approval?

You will generally need proof of income (pay stubs, T4s, or NOAs), proof of down payment, and identification. I will provide a specific list based on your situation.